What is a One Time Close (OTC)

New Home Construction Loan?

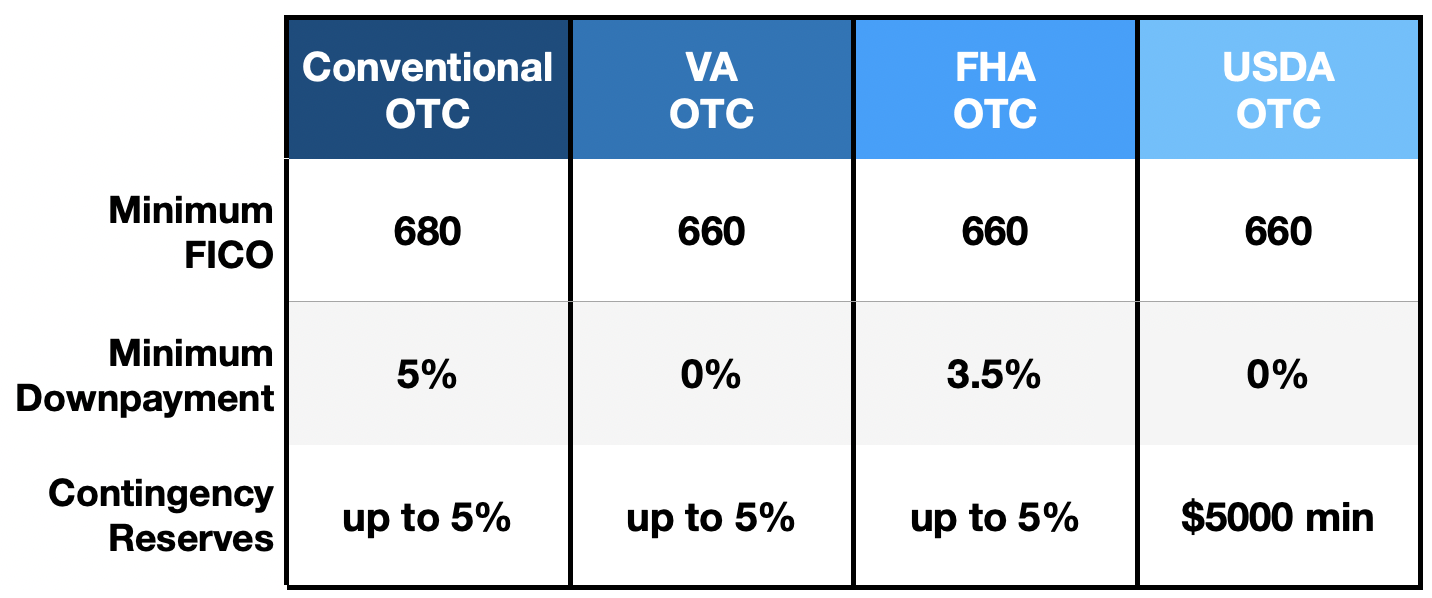

A One Time Close (OTC) New Home Construction Loan can enable borrowers to close on both the construction loan and permanent long-term financing simultaneously. As a result, both a builder and a borrower have added security. Before the job starts, the money to complete the project is in escrow, and the borrower knows the long-term interest rate. There are four potential options: (A) a Conventional OTC Loan, (B) a VA OTC Loan, (C) an FHA OTC Loan, or (D) a USDA OTC Loan.